Discover everything about RCM in GST – from reverse charge calculation to limits, rates, and compliance. Learn how to handle RCM entries, check GST reversal, and stay updated with 2025 notifications. Perfect for Indian businesses and taxpayers!

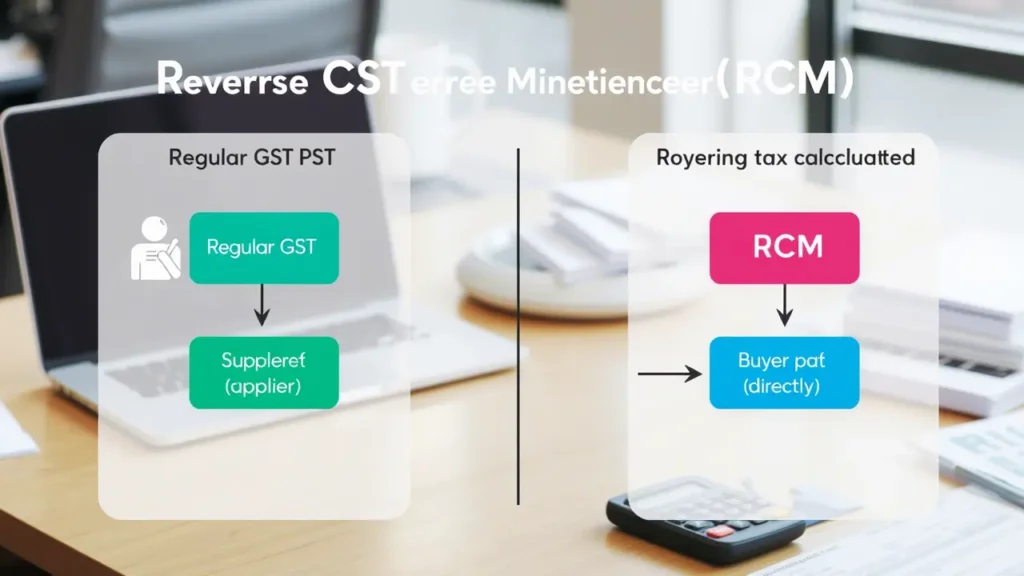

What is RCM in GST?

The Goods and Services Tax (GST) system in India has simplified taxation, but some concepts can still be confusing. One such term is RCM in GST (Reverse Charge Mechanism). If you’ve ever wondered, “Why do I pay GST even though I’m the buyer?”, this article is for you. Let’s break down RCM in simple terms, covering its rules, calculations, limits, and recent updates (as of 2025).

Understanding RCM in GST

Reverse Charge Mechanism (RCM) flips the usual GST process. Normally, the supplier pays GST to the government. But under RCM, the buyer pays GST directly. This applies to specific goods and services listed by the GST Council.

Example:

If you hire an advocate (a service under RCM), you (the recipient) must pay GST, not the advocate.

How Do You Reverse Charge GST?

Here’s a step-by-step guide:

- Identify if the transaction falls under RCM (check the GST Council’s list).

- Calculate GST on the invoice value.

- Pay the GST via your GST portal while filing returns (Form GSTR-3B).

- Claim Input Tax Credit (ITC) if eligible.

Note: RCM applies even if the supplier is unregistered.

How is Reverse Charge Calculated?

Formula:

GST Amount = (Invoice Value × GST Rate)

Example:

You buy ₹50,000 worth of goods under RCM at 18% GST.

GST = ₹50,000 × 18% = ₹9,000

What is the Limit of GST Reverse Charge?

The GST reverse charge mechanism (RCM) has specific thresholds to reduce compliance burdens on small transactions:

- General Limit for Services: For services procured from unregistered suppliers, RCM applies only if the total invoice value exceeds ₹5,000 per day. Below this, the recipient isn’t liable to pay GST.

- Example: Buying ₹5,500 worth of legal services in a day triggers RCM; ₹4,500 does not.

- Special Cases:

- Goods Transport Agency (GTA): RCM applies only if the consignment value exceeds ₹750 (post-2025, this applies pan-India).

- Imported Services: No monetary limit—RCM applies regardless of value.

These limits exclude cumulative transactions (e.g., multiple invoices below ₹5,000 on the same day are exempt). Businesses must track daily purchases and consignment values to avoid penalties. The GST Council periodically revises these thresholds, so check 2025 notifications for updates.

GST Rate for Reverse Charge

RCM rates vary based on the goods/service. For example:

| Service/Goods | GST Rate |

|---|---|

| Legal Services by Advocate | 18% |

| Goods Transport Agency (GTA) | 5% or 12% |

| Imported Services | 18% |

Note: Always check the latest GST notifications for updates.

Time Limit for GST Reversal

Under RCM, the GST paid on reverse charge must be deposited by the 20th of the following month in which the goods/services were received. For example, if you receive goods on March 15, the GST must be paid by April 20 while filing Form GSTR-3B. This deadline ensures timely tax collection and compliance.

Missing the due date attracts 18% annual interest on the overdue amount, along with penalties. The liability arises on the earlier of two dates: when you receive the goods/services or make payment to the supplier.

Example: A business procuring legal services on April 10 must pay RCM GST by May 20. As per 2025 updates, even small businesses must adhere to this timeline unless exempted under specific notifications. Regularly reconcile entries in GSTR-2B to avoid mismatches and ensure seamless ITC claims.

What is the ₹750 Limit for RCM?

The ₹750 limit applies specifically to Goods Transport Agency (GTA) services under RCM. If the invoice value for a single consignment is ₹750 or less, the recipient (buyer) is not required to pay GST under reverse charge. However, if the consignment exceeds ₹750, GST at 5% or 12% (depending on the GTA’s GST registration) must be paid by the recipient.

Example:

- A consignment costing ₹700: No RCM GST.

- A consignment costing ₹800: RCM applies (₹800 × 5% = ₹40 GST).

This threshold is per consignment, not cumulative. Businesses must track invoices carefully, as exceeding ₹750 even once triggers RCM. The rule aims to reduce compliance burdens for small shipments. As per 2025 updates, this limit applies pan-India, irrespective of transport distance or mode.

How to Check GST Reversal?

- Log in to the GST portal.

- Go to ‘Services’ > ‘Returns’ > ‘Returns Dashboard’.

- Check Form GSTR-3B for RCM payments.

What if the Supplier Has Not Paid GST?

Under RCM, your responsibility to pay GST remains unaffected even if the supplier hasn’t deposited their share. The law mandates that the recipient (you) must pay the applicable GST and report it in GSTR-3B. However, to claim Input Tax Credit (ITC) on this payment:

- Ensure the supplier’s GSTIN is valid and active (check via GSTR-2A/2B).

- Verify that the transaction is reflected in your purchase records.

If the supplier is non-compliant, the GST department may block their credits or initiate recovery actions. Meanwhile, you cannot deny RCM liability but can report the supplier’s default via the GST portal’s “Report Non-Filers” tool. Always maintain invoices and payment proofs to avoid disputes during audits.

Example: If a vendor fails to pay GST on raw materials supplied to you, you still pay RCM and claim ITC, but the supplier risks penalties.

Try Our Free Online GST Tools

How to Pass an RCM Entry in Accounting

Journal Entry Example:

- Debit: Purchase/Expense Account

- Debit: ITC Receivable (if eligible)

- Credit: GST Payable under RCM

Is RCM Refundable?

Yes, RCM GST is refundable under specific conditions. Businesses can claim refunds for RCM payments if:

- The goods/services are exported (zero-rated supplies).

- There’s an inverted duty structure (where input tax exceeds output tax).

- The taxpayer is eligible under the GST compensation cess scheme.

To claim a refund, file Form GST RFD-01 with supporting documents like invoices and shipping bills. The refund is processed within 60 days of application. However, refunds are not allowed for RCM paid on personal purchases or blocked credits (e.g., construction services).

Example: A textile exporter paying RCM on imported machinery can claim a refund if the final products are exported. Always reconcile RCM entries in GSTR-2B to avoid mismatches and ensure timely refunds.

List of RCM Under GST (2025 Update)

Goods:

- Tobacco leaves

- Lottery tickets

Services:

- Legal services

- GTA services

- Director services

RCM Notification Under GST

The GST Council periodically issues notifications to update RCM rules, ensuring alignment with economic needs and compliance efficiency. The 2025 RCM notification (No. 10/2025) expanded the scope of services under reverse charge, including IT freelancers, digital content creators, and certain B2B e-commerce transactions. Key highlights:

- Mandatory RCM for services procured from overseas digital platforms (e.g., cloud storage, SaaS tools).

- Revised thresholds: The ₹750 limit for Goods Transport Agency (GTA) services now applies pan-India, regardless of consignment size.

- Simplified compliance: Businesses must report RCM liabilities in Form GSTR-3B and GSTR-1 separately to avoid mismatches.

The notification also exempts SMEs with turnover below ₹2 crore from RCM on non-business purchases. Taxpayers must regularly check the GST portal for updates, as non-compliance attracts 18% annual interest + penalties. Staying updated with these notifications ensures smooth operations and maximizes Input Tax Credit (ITC) claims.

Also Read

- How to Claim GST Refund in 2025? Ultimate Guide for Businesses and Taxpayers.

- Reverse GST Calculation Formula 2025: Step-by-Step Guide

- How is GST Included in MRP? In 2025

Conclusion

Understanding RCM in GST is crucial for businesses to avoid penalties and maintain compliance. Unlike the regular GST process, RCM shifts the responsibility of tax payment from the supplier to the recipient, ensuring the government collects dues even when suppliers are unregistered or non-compliant. By mastering how reverse charge is calculated (based on invoice value and applicable GST rates), adhering to time limits (payment by the 20th of the next month), and recognizing critical thresholds like the ₹750 limit for transport services, taxpayers can navigate RCM confidently.

The mechanism also offers opportunities, such as claiming Input Tax Credit (ITC) on RCM payments, which reduces overall tax liability. However, vigilance is key—regularly checking the GST portal for reversals and staying updated with the 2025 RCM notifications (like the expanded list of services under RCM) ensures businesses stay ahead of changes. For instance, sectors like e-commerce and freelancing now face stricter RCM rules, emphasizing the need for proactive compliance.

Ultimately, RCM isn’t just a legal obligation but a tool to broaden the tax base and promote fairness. By maintaining accurate records, consulting professionals for complex cases, and leveraging GST’s digital infrastructure, businesses can turn RCM compliance into a strategic advantage. In a dynamic tax landscape, staying informed isn’t optional—it’s essential for sustainable growth.

FAQ About RCM In GST

When does RCM apply?

RCM applies when buying specific goods/services (like legal services) from unregistered suppliers.

Is RCM applicable for small businesses?

Yes, if they purchase RCM-listed items.

Can I avoid paying RCM GST?

No, it’s mandatory if your purchase falls under RCM categories.

How to know if a service is under RCM?

Check the GST Council’s list or consult a CA.

What happens if I miss the RCM payment deadline?

You’ll pay 18% annual interest + penalties.

Can I claim ITC on RCM payments?

Yes, if the purchase is for business purposes.

Is RCM applicable for imports?

Yes, GST is paid under RCM for imported services.

How often is the RCM list updated?

The GST Council reviews it annually.

Do I need to issue an invoice under RCM?

No, the recipient doesn’t issue invoices for RCM.

Are there exemptions for RCM?

Yes, for certain agricultural products and healthcare services.

Pingback: What Happens If GST Is Not Filed? Free Guide In 2025 - gstcalculatorpro.com

Pingback: Cement GST Rate 2025: Shocking Updates Every Builder & Homeowner Must Know! - gstcalculatorpro.com